Industry Update

The DGFT on 15th October 2020 came with a notification where they have put import of ACs with refrigeration under prohibited list. This prohibition increases the addressable market size for contract manufacturers significantly and is in continuation to government’s earlier moves to boost domestic manufacturing as discussed in the previous quarterly update.

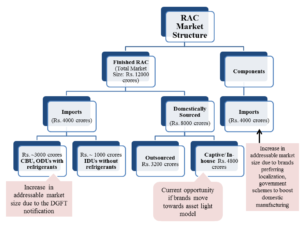

The below flow chart discusses the impact of policy and how it will increase the addressable market for OEMs like Amber Enterprise.

Source: Company Presentation, gunjankabra.com

The import ban opportunity size is 2.4 million units. Being a market leader in outsourcing with higher degree of backward integration, any increase in outsourcing will increase the addressable market size for Amber in a meaningful way. The uptake in volumes due to this policy is expected to reflect next year. Amber has a capacity of 4 million units and it sold approximately 3 million units in FY2020. For time being, the company has enough buffer capacity to meet the increasing demand.

As per the management guidelines, as the inverter AC got popular in usage, individual IDU imports started to decrease in last 4-5 years. In an inverter AC, the ODU and IDU are linked electronically and work in synchronised manner, so it is difficult for OEMs to import indoors and manufacture ODUs in India. Hence, this policy is expected to increase local manufacturing.

If the brands import units without refrigerants, then they will have to unpack it, fill the refrigerants at their locations, pack it again and then transport to the respective outlets. This hassle would incur cost of ~ Rs. 800-1000 per unit and that negates the benefits of low cost imports.

Going forward, as per the management AC players are re-visiting their strategies after this policy. The company has added 4 new clients (they used to import completely) on the RAC side and is in talks with other four prospective clients.

Company Update

Capex: There are two green field expansions in place coming up in Pune, operational in Q4 FY22 and another facility in Tirupati commencing in Q1 FY23, adding 1 million units to the total capacity.

QIP: Amber completed a QIP of Rs. 400 crores which will be used for:

- 275-300 crores would be used to meet the capex requirements

- 55 crores used for acquiring the remaining 20% stake of Sidwal

- The remaining Rs. 45-70 crores for capex in subsidiaries, debt repayment and working capital requirements.

Result Update

The results were sequentially better in some aspects but full recovery is expected in Q4 FY2021 as also mentioned in the previous update.

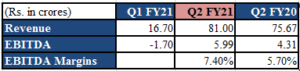

- Revenues

In Amber, volumes play an important role in the performance of the company. Any significant decrease translates into operating de-leverage for the company as explained below.

- Fall in Volume led to

2. Decline in revenue resulting in

![]()

3. Fall in EBITDA and Margins

- Recovery in component business

The revenue did increase qoq majorly due to rise in revenue from subsidiaries. The company experienced huge demand in the component business from the consumer durable space (Non AC Components) during the quarter.

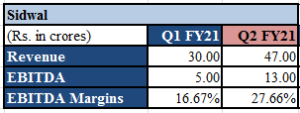

- Sidwal received new orders of Rs. 98 crores from DMRC and has a total order book of Rs. 350 crores which needs to be executed in next 18-24 months.

- Other Subsidiaries

PICL

ILJIN

EVER

- Expenses

The company’s cost optimisation measures and better product mix did reflect some kind of operating efficiency during the quarter.

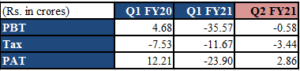

- PAT

The operating de-leverage explained above dragged down the profit yoy. It improved sequentially on account of higher revenues, better operating efficiency. Going forward, as channel inventory got normalised in Q2 FY21 as per the management, the company is expected to perform better in the next quarter and full recovery is expected from Q4 FY21.

- Export Opportunities

The China +1 strategy has presented export opportunities to the company. The company has started to supply its components (Motors and Heat exchangers) to the US and Middle East. On exports front in RAC market, China and Thailand are two large exporters accounting for almost 65 million units. China exports around 80% of the total and the rest is by Thailand. For RACs of 1.5-2 tonnes, Amber is at par on cost basis compared to China and Thailand. Some countries have FTA agreement, there the company is non-competitive. 1 tonne RACs is largely catered by China and the company is not yet competitive in that space. On the components side of the business, the company has become cost-competitive globally.

- Other Highlights

–Industry witnessed a decline of 33% in HY2021

–Capacity Utilisation was 45-50% in Q2 FY2021

–The company has set up an office in the US

–Net Debt of the company was at Rs. 178 crores

–Q3 FY2021 is expected to remain flattish and strong demand is expected in Q4 FY 2021

Key Takeaways and drivers for growth

- Going forward, Amber is expected to benefit from:

–Prohibition on import of air conditioners with refrigerants

–China +1 strategy and Aatmanirbhar Bharat (schemes initiated by government)

–Focusing on exports and component business

–New Expansions

–Rising share of Outsourcing as a theme

–Growing order book of Sidwal (high margin business)

2. The long term story looks intact considering the penetration of AC is very low in India and the company being the market leader is expected to get the majority of the increasing pie. But, I believe, volumes are integral to its performance. In short term, one should do that due diligence carefully. The recovery is expected from Q4 FY21. The next quarter is a seasonally weak quarter for the industry as a whole amd is expected to remain flattish.

Please find the below link for pdf file on the same.

Amber Enterpise India Ltd. Q2 FY21 Result Update

Disclaimer:

I am not a SEBI Registered Analyst. The views expressed therein are based on information available publicly/internal data/other reliable sources believed to be accurate. The information is provided merely for educational purpose only and in no way meant to be a stock recommendation.